Commentary

'OTT Affluencers' Wield Outsized Influence...And Welcome Advertising

- by Karlene Lukovitz @KLmarketdaily, August 13, 2019

It’s no secret that affluent consumers have a weighty influence on U.S. spending.

Specifically, although they represent only 20% of the population, households with incomes of $125,000 and over account for 60% of total household expenditures, according to the Ipsos research firm, which has been fielding its Ipsos Affluence Survey (IAS) for 43 years now.

Ipsos has also identified a subset of affluents who have even more disproportionate power in terms of influencing the purchases of others — dubbed “affluencers.”

Recently, the firm zeroed in on the OTT/streaming attitudes and behaviors of affluents — including “OTT affluencers” who are at the forefront of video and other content consumption through these still relatively new platforms.

Ipsos used its Spring 2019 IAS (24,987 respondent households at that $125K or higher income level) as a foundation, and then fielded a re-contacting survey in April (1,004 IAS respondents) to probe their “new TV” profile.

For comparative purposes, the researcher also fielded a smaller survey (209 respondents) of households with income under $125K.

While the results’ confirmation of affluents’ power may not be all that surprising, the magnitude of their impact on the current new-TV environment should certainly grab the attention of all platforms that are hoping to survive and thrive in the so-called “streaming wars” ahead, as well as every consumer brand advertiser.

For starters, 77% of U.S. affluents subscribe to at least one streaming service, versus 62% of those in the below-$125K population sample (which I’ll call “non-affluents,” for short), reported Michael Baer, senior vice president, head of audience measurement for Ipsos, in a recent webinar.

In addition, 56% of affluents subscribe to premium TV channels, compared to 37% of non-affluents.

Affluents also spend more than 20% more on video subscription services ($42.42 per month, on average, versus $34.83).

Nearly a quarter (24%) of affluents spend more than $50 per month on video subs, versus just 12% of non-affluents. Further, on average, affluents said they would be willing to pay $49.23 for streaming services — or about $7 more per month — whereas non-affluents said their top per-month spend would be just $2 more ($37.04). In other words, combined, affluents are willing to pay more than 30% more than non-affluents going forward.

These differences would be even greater if consumers who are paying zero for services were included in the calculations, Baer noted.

OTT Affluencers’ Impact

Ipsos measures affluencers over 22 categories, and has consistently found that they lead the way, particularly in categories that are undergoing transformation.

Category affluencers are far more passionate and engaged about a category than others, have very high purchase intent, are early adopters, and are five to 10 times bigger spenders in the category than non-affluents — which is why others look to them for expertise, of course.

In engagement, OTT affluencers are heavy binge watchers, indexing at 129. (Because binge-watching has become commonplace, that may not appear that high, but it’s significant, according to Baer.)

In purchase intent, they’re willing to spend an additional $9 per month — $2 more than the general affluents subset.

In early adoption, they index at 208 for “I’m always on the lookout for new shows.”

The capper on this pyramid: They index at an impressive 558 on “I often give advice to people on what to watch.”

OTT affluencers’ profile: They have a median household income of $184,000 (vs. $168K for “non-OTT affluencers”); a median age of 41 (vs. 48); and 29% are business owners (versus 11%).

They have a male/female ratio of 48%/52% (versus 54%/46%), and nearly half (47%) have children (under 18) in the household (versus 39%).

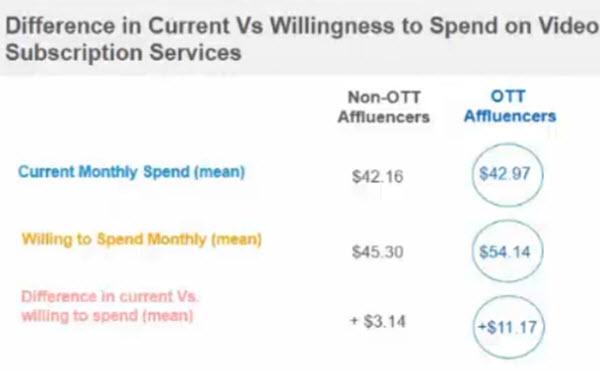

On average, they’re willing to spend $54.14 per month on video services, compared to $45.30 for non-OTT affluencers.

Further, 68% say they have the primary or final say in subscribing to video services, versus 48% for non-affluencers.

The kicker: Affluents across all categories — including OTT —"have a fundamentally different view of advertising than non-affluencers,” stresses Baer. “They don’t view it as an interruption; instead, they view it as another way to stay engaged and up-to-date on the category they’re passionate about.”

They agree with statements such as “Advertising helps me know what new products are available,” and “Brands with good advertising are higher-quality,” reports Baer.

When it comes to making viewing decisions, because they are active information seekers, OTT affluencers are more likely than non-affluencers to pay attention to recommendations from friends and family (63% versus 48%); advertising on television (54% versus 43%); family/friends’ posts on social media (39% versus 25%); magazine/newspaper articles (26% versus 18%; and ads on social media sites (25% versus 13%), among other factors.

They’re not much more apt to use the guide/menu (33% versus 31%), which “makes sense, because that’s a more passive” means than the others, points out Baer.

Nearly all OTT affluencers subscribe to at least one paid video streaming service (88%, versus 70% of non-OTT affluencers), and 68% currently pay to subscribe to some premium TV (versus 48% of non-OTT affluencers).

Fully 80% of OTT affluencers agree that “paying for content that I value is worth it” (they index at 161 on this) versus 7% of non-OTT affluencers.

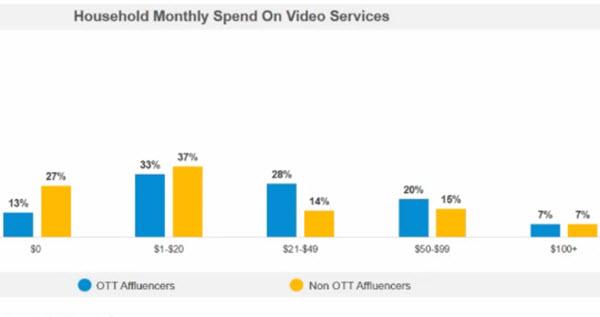

More than half (55%) are spending more than $21 on paid streaming services, versus just 36% of non-affluencers (and just 13% are spending nothing on these services, versus 27% of non-affluencers).

And while OTT affluencers’ current average sped per month on video services isn’t much higher than non-OTT affluents’ ($42.97 versus $42.16), they say they’re willing to spend more than $11 more per month, versus just $3 for non-OTT affluencers (see chart at top).

OTT Affluencers Watch More

In terms of viewing behavior, OTT affluencers spend more time viewing services, and they watch a wider variety of content, with a particular penchant for drama, comedy, reality and movies.

And when considering subscribing to new services, they say they “want it all,” says Baer.

They are most differentiated from other affluencers and non-affluecers by their valuing of original content, and least differentiated when it comes to live television (news and sports), he notes.

And They Still Buy Cable…

The good news for “traditional” TV: Despite all of the above, 63% of OTT affluencers still pay for cable- or telco-provided services (18% have satellite).

The research goes into considerably more detail on affluents’ content preferences, services spending, viewing behaviors and attitudes toward OTT… but I’ll let you watch the webinar yourself to absorb all of that rich information.

My point here, again, is that brands and platforms alike that underestimate the power of affluents in general, and OTT affluencers in particular, do so at their peril.

Karlene Lukovitz is editor of MediaPost's "Digital News Daily" and writes the weekly "Video Insider" and "Advanced TV Insider" columns. You can reach her at karlene@mediapost.com.

Karlene, no one can argue about the buying power of affluent Americans relative to those with lower incomes. That's a given as is the fact that affluents are more likely to be streamers. And, not surprisingly, many marketers consider affluents to be better prospects for their products or services. However, the hidden message in this study ---one that is implied by the admonition not to underestimate the power of affluents as doing so might be perilous----is that advertisers should pay much more attention to streaming media. Which is fine, but the same study reveals that many affluents also have "Pay TV", meaning that it's not an either or situation. More likely a mix of both for most advertisers ---with "TV" probably getting the lion's share of the dollars commensurate with its overall viewing tonnage and reach edge. I also find it difficult to accept the implication that affluents are more receptive to ads ---TV commercials, I assume---than others. Sure, they, like every body else, respond best to ads that are of interest to them but every study I have seen finds that, overall, lowbrows are more accepting of ads---especially TV ads--- than highbrows.