A new study from Deloitte confirms that Boomers still hold the cards when it comes to investable wealth as reported by the Wall Street Journal on Nov. 10, 2015:

“The baby boomers,

those who are between 51 and 69 this year, are currently the wealthiest group and they will retain that spot until at least 2030, according to the report. Boomers hold about 50% of the total wealth in

the U.S. now and they are expected to peak at 50.2% by 2020.”

The total amount of wealth in the U.S. is expected to grow from $72 trillion today to $120 trillion by 2030.

Boomers currently hold $36 trillion in wealth that needs a home and proactive management. The big investment companies have been all over the Boomer market for years with specific campaigns. They have

deployed aggressive marketing programs and online/offline educational content to help Boomers make informed decisions about their retirement planning and wealth management. And, to build long-term

customer relationships.

advertisement

advertisement

However, the large firms can’t service every Boomer financial need. What about their local and regional banks? Earlier this year, Gallup did an in-depth study of Boomer engagement with traditional banks. The findings point to some real

opportunities because Boomers use multiple financial institutions for various products and services.

“Among boomers with mortgages, for example, nearly four in 10 (38%) say

they have mortgages with the same institution that handles their primary banking; slightly more than two in 10 boomers with investment accounts (21%) say they use their primary bank for investment

services. The upshot is that when it comes to investing their wealth, the vast majority of boomers aren't working with their primary bank.”

A previous Gallup study found

that Boomers have a lot of ambivalence about their banks; only one in three is fully engaged with their primary banking provider. But two in 10 are actively disengaged, and nearly half (46%) are

indifferent toward their primary financial institution. This type of passive loyalty suggests that there are customers for the taking if they can get them to switch. It also points to a lack of

emotional connection with their primary bank.

To capture this opportunity and increase share of wealth banks need to think differently and retool their approach to marketing

and advertising. For example, here in the Boston area, banks do quite a bit of traditional advertising using broadcast, print, outdoor, online banners and search. Banks focus mostly on one-way

interruptive messaging and have not yet fully embraced the new world of conversational and personalized marketing where brands are co-created and shared. They tend to be laggards in the areas of

content marketing and social media outreach. The local bank brands tend to be undifferentiated for the most part, and the messaging is often about rates, deals or free checking for general customer

acquisition. That’s all fine and clearly necessary, but, as Gallup found, there

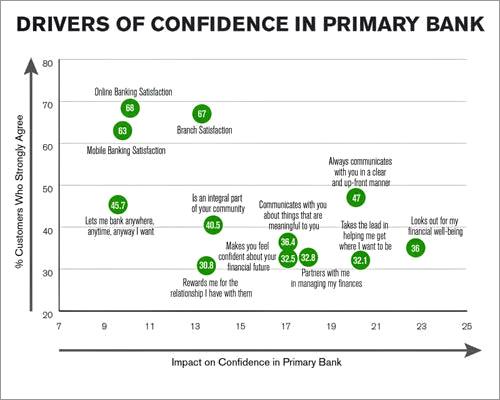

are drivers that help drive customer engagement and confidence.

Looking at the data, it appears that there is an opportunity to engage Boomers in a new way to help them

manage their finances as a partner. Banks can move away from being seen as just a place to conduct transactions by building emotional ties that will bind a customer for the long term. Essentially,

turn passive customers into active loyalist and vocal advocates for the brand. Much of bank advertising is focused on the top of the sales funnel and attempts at generic brand building. The Gallup

studies suggest that more effort is needed to create deeper bonds leading to up-sells/cross-sells with current customers.

By creating educational content (blogs, e-books,

videos, interactive tools, events) and outreach programs to work with Boomers on their financial wellness, banks can go a long way to capturing a customer base that currently relies on a number of

financial intuitions. Additionally, banks need to create specific multi-channel marketing campaigns that target Boomers with a clear message about their retirement planning and security. The

opportunity is there for the bank that redeploys just a small portion of their budget from traditional ads, and invests in some new media thinking across the full spectrum of of the customer

journey.