Based on the

technical definition of a recession, the Great Recession lasted 18 months and ended in June 2009, exactly five years ago. That was the point at which the U.S. economy stopped contracting.

Based on the

technical definition of a recession, the Great Recession lasted 18 months and ended in June 2009, exactly five years ago. That was the point at which the U.S. economy stopped contracting.

Focusing on the amount of time required to attain pre-recession “high-water marks” on key business, investment, and people metrics, it’s clear that the recovery has been uneven

and continues to be a work in progress.

There are now several indications, including last week’s release of the Conference Board Consumer Confidence Index (May 2014), that the U.S.

economy is moving in the right direction and the final pieces for a more complete recovery are falling into place.

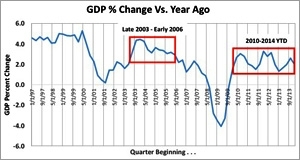

Gross Domestic Product

Perspective

The GDP has shown improvement since hitting bottom during the second quarter of 2009, but year-over-year gains have been ranging from 1% to 3% — in comparison to the

3% to 4.5% increases observed between late 2003 and early 2006.

advertisement

advertisement

The Corporate Perspective

The impact of the recession for national

advertisers varied by industry and company. Apple experienced dramatic uninterrupted earnings growth throughout the recession. Well-known recession resistant companies like McDonalds,

Colgate-Palmolive, and Walmart also experienced uninterrupted earning growth (at far lesser rates than Apple). It took companies like IBM and Intel two or three years to recover to pre-recession

water-marks. Then there are several major advertisers that, according to the Value Line Investment Survey, have not yet achieved the levels of financial performance achieved pre-recession.

Major media companies experienced similar variation in performance. Google, Discovery Communications and Comcast experienced uninterrupted earnings growth throughout the recession. Companies

like CBS, Disney and 21st Century Fox rebounded to pre-recession high-water mark levels within three to four years.

The Investor

Perspective

What about the price of common stock? The value of a share of common stock is typically based on a combination of hard financial metrics from income statements (such as

revenues and earnings) and balance sheets, estimated return relative to alternative investment options and the risk tolerance of the investor.

The recession brought a reduction in investor

risk tolerance. Stock prices declined to compensate for an increase in perceived risk -- which extended the amount of time required for common stock valuations to return to their pre-recession

levels.

It took the S&P 500 Index five years, five months to return to its pre-recession high-water mark level. Of the media companies mentioned above, Disney was among the fastest to

achieve its pre-recession high-water mark, two years, six months. CBS rebounded within four years and 8 months. Comcast rebounded within five years, two months. Twenty-First Century Fox rebounded

within five years, six months.

The Consumer Perspective

The Consumer perspective is most important because consumer spending accounts

for about 70% of the Gross Domestic Product. To gauge what is going on in the mind of the consumer, this analysis makes use of the Conference Board Consumer Confidence Index, a composite of consumer

assessments of the present situation and expectations for the future.

Over the previous two recoveries, i.e. the late 1990s and mid-2004 through mid-2008, consumers reported

being positive about the present situation (red line) but with more modest expectations for the future (green line). In both of these recoveries, the present situation far

exceeded expectations for the future.

By comparison to those recoveries, the current recovery has been shallow. The composite consumer confidence index (blue) is far below its

pre-recession high-water mark and we have had a condition that, except for transitionary periods, is unprecedented within recent history with the expectations for the future index exceeding the

present situation index.

The composite consumer confidence index is now on an upward trend. The trend has been driven by improvements for both the present situation index

and the expectations for the future index. We are at a point where the gap between the present situation index and the expectations for the future index is narrowing; a possible

indication that the last piece of the recovery is beginning to fall into place.

These trends are no doubt linked to progress with common stock valuations, an improving employment and jobs

picture (notwithstanding concerns over reduced wage levels and part-time employment for those returning to the work-force) and improvements in real-estate values.

The Employment and Jobs

The unemployment picture has improved – at slightly above 6%, it is trending in the right direction, now 1.9 percentage points above the May

2007 trough. Non-farm employment is close to achieving the January 2008 level (subject to reduced wage and part-time concerns).

Real Estate Values

The Case-Shiller

Home Price Index is showing evidence of a recovery in home prices, an important component linked to “wealth” perception. On a national basis, about 40% of the gap observed between

the Q2 2006 high-water mark level and the depressed levels observed between late 2011 and early 2012 has been closed. Of course, actual progress on this front varies on a market by market basis.

In summary, there are indications that the economy is moving in the right direction. Record levels for the S&P 500,

decreasing unemployment, increasing employment, and the restoration of real-estate values (and “wealth” perceptions) are all contributing to improvements in consumer confidence as measured

by the Conference Board. With continued improvements in these areas, the economy is poised for a final “consumer-based” recovery.