After nearly half a century of working

with a chip on my shoulder, GroupM Global President of Business Intelligence boosted my self-esteem when she kicked off a press briefing ahead of this week's release of her mid-year ad industry

forecast update.

"We have some trade reporters and some non-trades on the call," Scott-Dawkins began, adding, "My argument is that pretty much everyone these days is a trade reporter, because

if you’re covering anyone of the largest companies in the world, you are talking about advertising."

She went on to back her argument up by citing some pretty daunting stats underlying

one of the central themes of GroupM's new forecast: consolidation.

"Google, Apple, Microsoft, Amazon, these are all companies that sell advertising, and Nvidia sells the chips on which these

companies provide their advertising services," she explained.

advertisement

advertisement

Obviously, Scott-Dawkins was speaking euphemistically about everyone being an ad trade reporter, even if she was just

referring to members of the general press, much less media planners and buyers like you.

Most of you probably write better than me, and certainly wouldn't use a gimmicky anecdote like this to

make a point. But many of you probably also know I can't resist an invitation to do so when it's presented to me.

That said, there is a serious point in Scott-Dawkins quip, and all you need to

do is look at the GroupM data below to consider the magnitude of it.

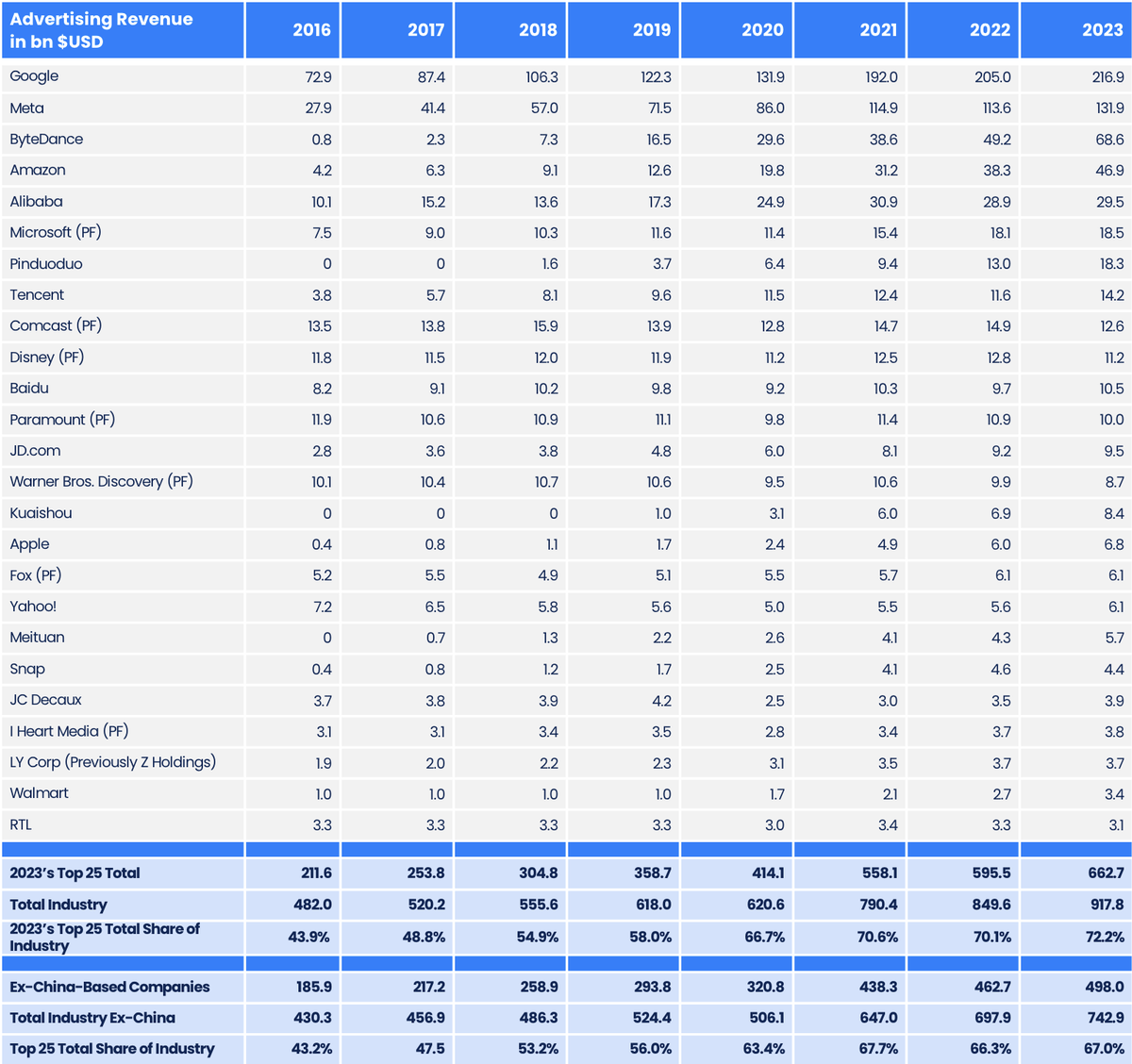

Yes, it shows how the share of ad industry spending increasingly is consolidating among a handful of its biggest players,

but the biggest among them also happen to be the biggest companies in the world.

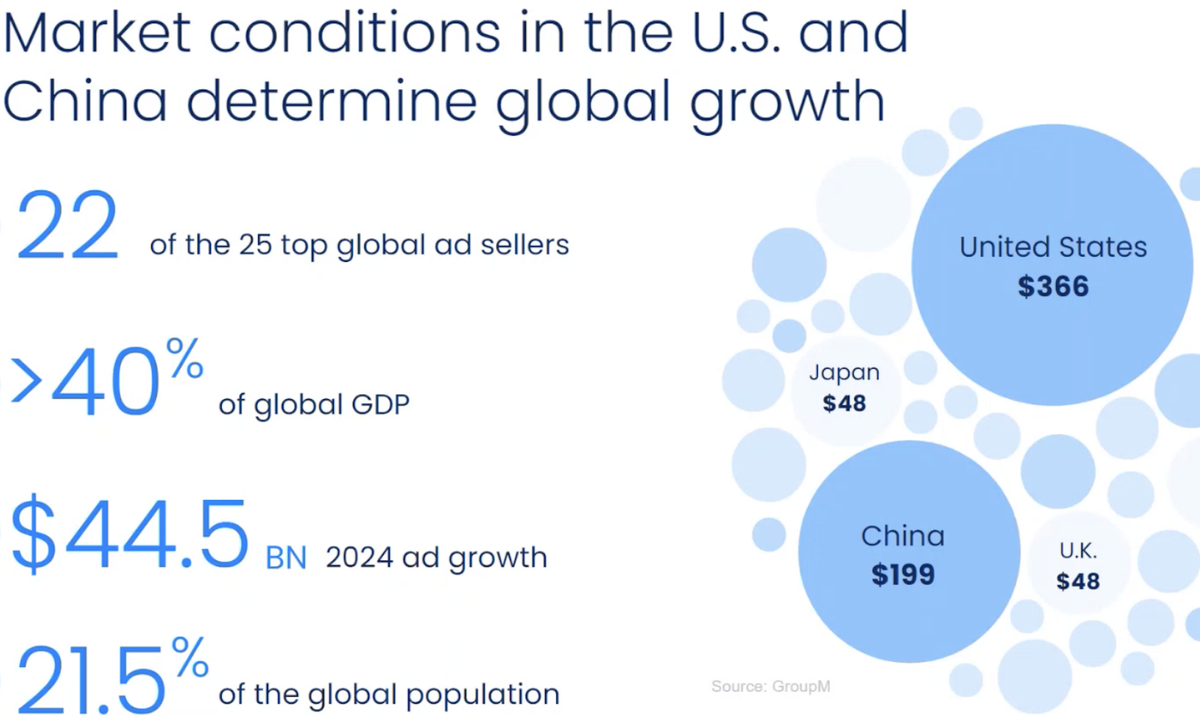

If you include AI chipmaker Nvidia, the five largest companies in the world

are based in the U.S., and if you go deeper down the list, most of them are based here or in China, which relates to GroupM's second big visual data point:

The good news for the ad industry is both of those two giant ad markets are surging, which is a big

part of GroupM's multiple percentage point upgrade for the global ad economy this year.

The bad news is it means advertisers, planners and buyers are more beholden to an increasingly

consolidated supply chain than ever before.