GroupM estimates revenue from search advertising will grow 5.3% in 2024

to reach $206.4 billion worldwide -- rising to $269.6 billion in 2029.

Search will account for 20.9% of total ad revenue in 2024 -- a share that the agency predicts will remain stable during

the next five years.

The top five companies -- Google, Meta, ByteDance, Amazon, and Alibaba -- accounted for 53.8% of the 2023 total.

Most realize that 2024 will become a

transformative year. Google, Microsoft, Baidu and others will continue to build AI-enhanced search products, forever changing the way marketers market and advertise products and services.

The

technology not only analyzes creatives and targeting, but also video. YouTube used machine learning to analyze more than 8,000 ads posted to its platform this year. Then it surfaced the top five key

creative trends such as underrepresented voices, celebrating individuality, reinforcing community, sparking wonder, and building trust.

advertisement

advertisement

Not all brands are comfortable with generative AI (GAI)

technology. Lucidworks made that clear in a global study it conducted recently among more than 2,500 participants.

All participants were affiliated with organizations actively pursuing

generative AI initiatives and were involved in decision-making, implementation, and use of generative AI tools.

Lucidworks' study is intended to forge an understanding of key areas of GAI

investments and how advanced organizations adopt the technology.

It evaluated 80 GAI best practices across five categories and identified four stages of generative AI development. This year

the focus is much more about leading the competition, as the hype turns into reality and the technology matures to the point of reducing errors in creative design, media buying and targeting.

The study evaluated 80 generative AI best practices across five categories and identified four stages of generative AI development. The research findings support probable generative AI "next steps"

that are specific to various industries and provide valuable insights for companies looking to advance their generative AI initiatives.

Key findings included flattened spending, indicating

more thoughtful planning, deployment delays that stall anticipated return on investment, implementation costs raising alarms, practicality driving GAI adoption, and leaders investing in future-proof

AI alternatives.

Interesting insights point to spending trends. Services show 70% of organizations plan to increase spending during the next 12 months, followed by B2B at 68% and B2C retail at

64%.

Healthcare and hospitality show only 51% and 50% of businesses plan to increase their investment in the coming months. Manufacturing also is being more conservative. Their planned

spending is down to 58% from 93% in 2023.

The survey also examined financial benefits — profit and revenue — and soft benefits — customer satisfaction, employee satisfaction

and competitive position.

The financial benefits of implemented projects have been dismal. Some 42% of companies have yet to see a significant benefit from their GAI initiatives.

The

report highlights a key reason for the slowdown in adoption rates. Marketers are in the learning stages of the technology and success rates of getting projects beyond the initial stages are few and

far between.

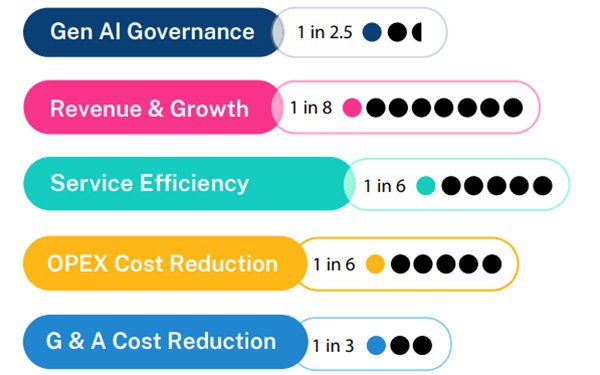

Companies were asked how many initiatives progressed past pilot programs or proof-of-concept and became fully operational.

Only 25% of planned generative AI investments

have been fully implemented so far. Tech and retail companies report the greatest success. The tech sector leads with the most deployed initiatives across all industries and half have already realized

financial benefits, despite an above-average level of delays.

Retail comes in at a close second and has achieved the highest deployment of revenue and growth initiatives.