They say April is the cruelest month, but if you are interested in engaging and marketing to teens, it should be the month you look forward to all year. Why? Because April is the month

Piper Jaffray issues its “Taking Stock with Teens” annual collaborative consumer insights report. I came

across this several years ago and have found it to be an incredibly interesting and really useful read.

Piper Jaffray has been doing this research since 2000 and this has

given them a tremendous amount of data on teens, their brand preference and spending patterns. For this year’s report, there were 6,500 respondents, with an average age of 16.5 years.

Thirty-nine percent of respondents work part time. The survey breaks teens into two groups: upper-income, of which there were 1,300 respondents with an average household income of $101,000; and

average-income, of which there were 5,200 respondents with an average household income of $53,000. Data on both groups was collected through a combination of classroom visits and electronic

surveys.

advertisement

advertisement

The report is, as always, a mix of the insightful and the mundane. One of the most interesting and important findings is that teen spending overall is down. Among

upper-income teens, total spending is down 10% from April 2015. For average-income teens, the year-over-year spending drop is 4%. My favorite of the mundane findings: “denim appears to be

working.” As if it ever wasn’t! (Ignoring, of course, its awful acid-washed phase ...)

The report deep-dives into three big areas of teen spending: fashion and beauty

(which accounts for 38%), restaurants (which represents 22%) and movies and devices (which account for 27%). While there is interesting information in each of the categories, movies and streaming is

in many ways the most interesting because it shows some of the areas of greatest change.

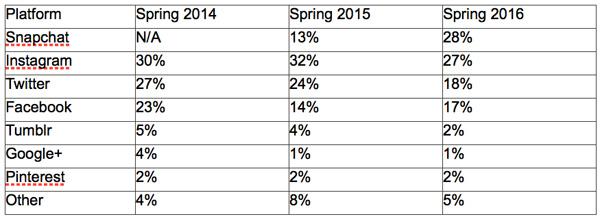

First among them is the rise of Snapchat. Two years ago, Snapchat didn’t even appear

on the list of most popular social networks among teens. Today, it is the preferred social network for 28% of respondents, placing it in the top spot. Here’s the breakdown, over the past two

years, of teens’ preferred social media platforms:

The takeaway here isn’t that Snapchat is awesome (even though it is) but that there is constant

volatility in the teen social media space. While brands must find ways to tap into what teens are gravitating to in a given moment, they must be flexible enough not to become so entrenched in a given

platform that they’re unable to move quickly when another new service crops up and rises to the top.

A funny finding is what Piper Jaffray refers to as the “circle of

life” for teenage boys: food (20% of spending), clothing (15%) and video games (13%). Annual spending on video games is now at $214, the highest it has ever been. This would allow for just three

and a half new release console titles. Given the list of AAA games released in a year, one has to imagine that, as with parental contributions to spending in other categories, games are being

purchased on behalf of teens by others.

The report looks at streaming video and found, not surprisingly, that streaming dominates. One media category that the report

doesn’t explore — and one which is near and dear to the hearts of most teens — is music. It gets lumped in with movies, where together they account for just 5% of spending, down from

6% in the Spring of 2015. It would be interesting to have a clearer and better understanding of how teens are accessing music and how that is changing. One imagines that streaming dominates in this

category as well, but which service dominates? Are teens piggy-backing on family accounts? Perhaps a future report will explore this area in greater detail.

Overall, the report is

an interesting read. It offers a detailed glimpse into the spending behaviors and brand preferences of today’s teens. Anyone interested in developing a clearer view of teens needs to make this

report a central part of their annual rite of spring.