Bain publishes a good analysis every year of

so-called insurgent brands in the U.S. FMCG (fast-moving consumer goods) market. For the past few years, these small brands have captured a disproportionate share of annual growth.

This

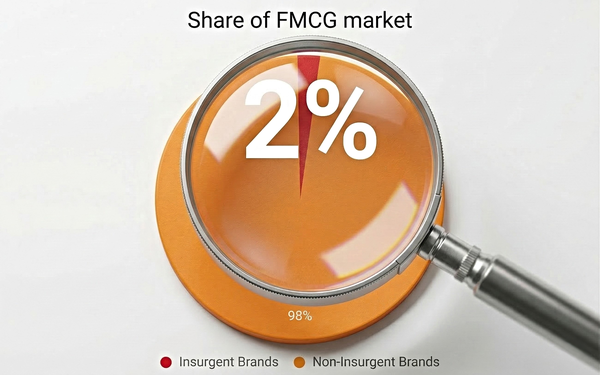

year’s analysis reports that in 2025 insurgent brands accounted for 36% of

aggregate growth across all FMCG categories, which seems pretty impressive given that they comprise an aggregate share of less than 2%.

But this headline-grabbing factoid leaves the

follow-up question hanging: 36% of what?

Bain notes that U.S. FMCG grew less than 2% in aggregate in 2025. Let’s work with that. To make the math easier, let’s call it an

even 2%. Thirty-six percent of that is 0.72 percentage points. Mind you, that’s not the average growth rate of insurgent brands -- that’s different multiplication. This figure is the chunk

of aggregate growth accounted for by insurgent brands.

advertisement

advertisement

We can put this chunk in perspective by comparing it to other chunks. In particular, the chunk of aggregate FMCG growth that

occurs naturally as a function of household growth (or alternatively, population growth).

From an analysis of ten years of global FMCG data that was published in 2022, Worldpanel found that half of annual FMCG brand growth comes from household growth. In other words, brands can get a lot of "money for

nothing," to paraphrase Dire Straits, merely by getting their fair share of the new buying that happens because there are more people in the category each year. That’s growth, but not real

growth.

Let’s push this illustrative parsing a bit further. My reverse engineering of the math gets kind of stretchy at this point, but it’s close enough. If only half of

the 2% aggregate FMCG growth reported by Bain is real growth, or growth not accounted for by population growth, that 2% gets chunked up into a 1.0 chunk for household growth, a 0.36 chunk for

insurgent brands growth, and a 0.64 chunk for established brands growth.

The takeaway is telling. Household growth, not insurgent brand innovation, is the dominant driver of FMCG

growth.

Innovative insurgent brands may enjoy outsized growth relative to their market share, but real growth for both insurgent and established brands is much weaker than the growth from more

households. This is a treacherous demographic dependency, which is playing out already.

McKinsey found slowing population growth to be one of the

three reasons why the global FMCG CAGR (compound annual growth rate) dropped from 9% over the 2001-2012 period to 2% over the 2013-2019 period.

Other analyses have shown that in the years immediately after COVID, price increases powered

top line growth for global FMCG brands, masking the underlying demographic softness in unit volume growth.

Certainly, there is a lot that established brands can learn from insurgent

brands. Insurgents are innovating more quickly and using social commerce channels more effectively. They are tapping into high-interest health benefits more convincingly -- especially things like

clean, organic, natural, high-protein and low-alcohol. And they are adapting to AI search and discovery at warp speed.

But as big of a threat as insurgent brands represent,

established FMCG brands have a bigger challenge on their hands. Their categories are either barely ahead of, or falling behind, household growth, as detailed analyses continue to show.

Simply put, their categories are flat or

declining. Established FMCG brands face scale risks that many Cassandras say are existential. At the very least, they are locked into a spiraling and commoditizing share battle with insurgent

brands.

The best way to win a share battle is to grow the category, not to try and tighten a death grip on competitors. This is what established brands need to do -- grow their

categories. The lessons to take away from insurgent brands should be lessons that benefit the entire category.

It’s not about outspending insurgent brands at what they do

better. That’s a hard row to hoe. Nor are they outracing household growth either. Rather, it’s about the simple truth that a rising tide lifts all boats.

Too many

established brands are chasing their tails trying to match or outwit tiny insurgent brands when instead they should be investing in the kind of big picture strategic work it takes to find new spaces

in which to grow their categories, and thereby themselves, too.

Not that this is easy. Three headwinds are working against FMCG categories these days.

The first is AI. As I

have noted in my last two columns, AI can send brands down dead-ends and consumers are using AI to hack brands and brand value. But AI is the future. As others have noted, side-by-side with figuring out future new spaces is figuring out the future of marketing.

The second

challenge is affordability -- it doesn’t matter how consumers discover or get to brands if they can’t afford them to begin with. Affordability is more than price. It’s share of

wallet. As I have explored in several of my regular "Charts of the Week" this year, affordability is mostly a share-of-wallet

issue occasioned by skyrocketing housing and healthcare costs.

On an inflation-adjusted basis, FMCG prices are largely unchanged. There is just less

left over once housing and healthcare have taken an ever-bigger bite each month. It is not too unfair to say that the biggest competitor of FMCG brands these days is housing and healthcare. It’s

those expenses that put the squeeze on everything else. Hypervigilant spending is the result.

Finally, household structure is

continuing to upend the structure of consumer demand. Demographic shifts are the single most important macro force. Household needs arise from household structure, so changes in structure give rise to

changes in needs. Most established FMCG brands hail from an era when household structure looked much different.

Today, households are singles or cohabitating couples or child-free

marriages or multigenerational or older mothers, not young married couples with children. It’s Gen Z on the way up, Millennials into late middle age, and Boomers on the way out. It’s young

women with more education and young men in skilled trades. It’s a shift of who’s at home with the kids and who’s doing the cooking. Just to mention a few big changes.

Established FMCG brands must update their basic understanding of a marketplace that is moving away from their basic value propositions --technologically, economically and demographically.

Sure, insurgent brands are more fleet of foot in this rapidly evolving landscape of demand. But it is established brands with the heft and muscle to move categories.

What insurgent

brands are up to is an input into a strategic reappraisal, but not the be-all and end-all of strategy. Insurgent brands are big in some ways, but they are not that big upon closer scrutiny. A lot of a

little is still not enough.

Established FMCG brands must follow big opportunities, not dash after slim pickings. The strategic imperative of this moment is growing the category.