The subscription video-on-demand market

has experienced “staggering” disruption since Disney+ launched in November 2019 — and the growing number of players continued to shake things up through this year’s first

quarter.

With Discovery+ and Paramount+ — the last of the major new premium streamers (for the moment, at least) — in the game as of fourth-quarter 2020, total U.S. subscriptions

in Q1 rose 24% on a year-over-year basis, and 6% versus Q4, according to Antenna.

The continued strength of the collective growth curve in the U.S.

— without factoring in what we know to be considerably more robust growth in international markets — is in itself pretty remarkable.

advertisement

advertisement

As the chart at the top of the page

shows, over two years, since Q1 2019, total U.S subscriptions have leapt by 64%.

As for the players, while Netflix continues to downplay the impacts of competition on its business, those two

years have seen the leader of the pack’s U.S. share plunge from 50% to 31%, according to this data.

In Q1 2019, before the advent of Disney+ and the other big launches, Netflix

accounted for three out of four U.S. streaming subs. But with subscriptions volume growth of just 8% since that time, its dominance, while still pronounced, has definitely lessened: It now accounts

for one out of two U.S. streaming subscriptions.

In addition, No. 2 U.S. SVOD Hulu has seen its share dip by 8 points, to 20%, over the period.

The four other premium SVODs that

were in-market two years ago — HBO Now (now HBO Max), Showtime, Starz and CBS All Access (now Paramount+) — still command about one in four subscriptions. But to maintain that share level

in the face of new competition, they have had to scale up significantly, achieving 100% growth during the period.

Disney+, Discovery+, Peacock and Apple TV+ now account for 22% of all

U.S. subscriptions. Disney+ has driven 44% of all category growth since Q1 2019.

As we know, the growing array of streaming choices has accelerated cord-cutting. The cable and satellite MVPDs

representing 95% of the market collectively lost a record 5.9% of their subscribers last year, versus 5.2% in 2019, according to Leichtman Research Group.

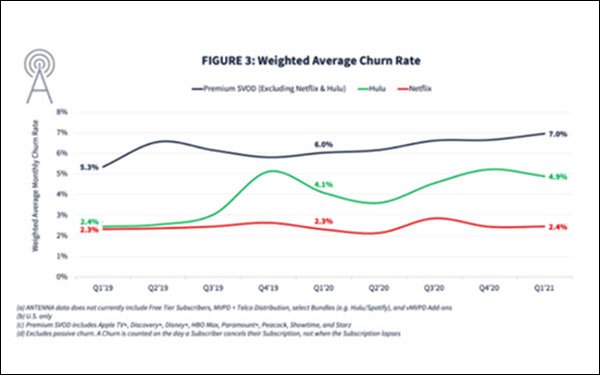

But here’s where

Netflix continues to have a crucial edge: While other services has experienced growing churn as the field of choices has widened, Netflix's customers have remained highly loyal.

Over the last two years, the premium SVODs

excluding Netflix and Hulu have seen average monthly subscriber churn rise from 5.3% to 7%.

Hulu’s churn rate has doubled, from 2.4% to 4.9%. That in part reflects pricing.

Its churn rate leapt to over 5% in Q4 2019, coinciding with Hulu’s raising the price of its Hulu Plus Live TV service for the second time that year. Hulu’s inclusion in the Disney+ bundle

and other factors, including promotions, no doubt also played roles in its churn trends over the period. But growing competition was also one a factor in the mix.

Meanwhile,

Netflix’s churn rate has barely budged, rising by a miniscule 0.1% over the eight quarters.

Netflix also leads the industry in resubscribe rate — meaning it’s more

likely than its rivals to win back subscribers who cancel.

That’s a heap of change in two years.

And, as Antenna notes, the race is bound to get more interesting in the coming

months, as the more recent entrants gain their footing, and the various players implement, adjust and perhaps shake up their various programming, pricing, bundling and distribution.