Perhaps fueling evidence for a healthier upfront

advertising market, national TV scatter advertising revenues continue to see decent gains in April -- at high-single digit percentages.

Standard Media Index, which culls 80% of national U.S. media

spend from five of six media agencies, said scatter advertising revenue rose 8% in April -- 13% for cable networks and 1% for broadcast networks. This follows national TV’s March scatter revenue

results which improved 11%.

Looking at scatter and upfront dollars from deals made in 2015, national TV advertisers spent 6% more revenue in April versus a year ago. Broadcast networks grabbed

7% more revenue from upfront deals; cable networks took in 10% more in upfront revenue. All national TV upfront revenues in April are up 9%.

SMI says this is “promising sign for both

cable and broadcast networks even as TV viewership continues to slide.”

advertisement

advertisement

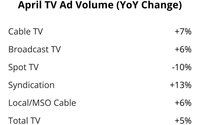

Total television -- national TV, spot TV, syndication and local cable -- climbed 5% in revenue in April versus a

year before.

Overall, U.S. media revenues rose 7% in the month -- with digital media revenues continuing to be the best performer, up 15% over the same month a year ago. Three key digital

areas continue to soar -- social media, 59% higher; video, 31% more; and digital ad networks/exchanges, 26%.

Out of home was also a big performer -- gaining 12% in the month. Down-trending

media segments: magazines, 5% lower; newspapers, falling 15%; and radio slipping 1%.

Best performing advertiser categories were quick serve restaurants (up 44%); prescription pharmaceuticals

(34% higher) and automotive vehicles and dealerships (adding 22%).