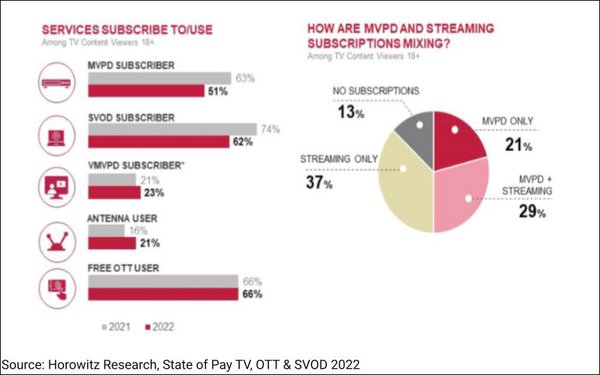

Just half (51%) of U.S. TV content viewers currently

subscribe to a traditional cable/satellite service, while nearly four in 10 (37%) now rely solely on streaming, according to a new report from Horowitz Research.

Pay-TV subscription

penetration is down from 63% in the same survey in 2021, and 81% in 2020, while streaming-only penetration is up from 30% in 2021.

Yet, even as streaming’s share and the number of

subscription-based video-on-demand (SVOD) subscription services have grown, SVOD penetration is down slightly.

In the 2021 study, 74% of viewers said they subscribed to at least one SVOD; this

year, that’s down to 62%. (An additional 10% have access to additional SVODs by sharing passwords.)

“It seems the streaming honeymoon is coming to an unavoidable end,”

asserts Adriana Waterston, chief revenue officer and insights and strategy lead for Horowitz. “What seemed like a fantasy come true [for viewers] — thousands upon thousands of hours of

top-notch content available on demand for almost no money and few, if any, ads — was never going to be a sustainable business model, given what it costs to produce and acquire great

content.”

advertisement

advertisement

According to Horowitz, the SVOD penetration dip is due in part to a drop in Netflix subscriptions.

Meanwhile, the number of TV content viewers using free, ad-supported

sources (FASTs) and free antenna reception is unchanged at 66% — on par with SVOD users.

In what’s likely no coincidence, the amounts that consumers are paying per month for

streaming services is on the rise.

On average, streaming services subscribers (including those with SVOD and/or virtual multichannel video programming distributors/vMVPDs like Sling TV or Hulu

Plus Live TV) now report spending $75.80 per month on their services — up by $26 per month from last year’s reported average spend.

The cost increase has been driven by adoption of

a growing number of new services, such as Discovery+ and Paramount+ (both launched last year), and price increases from Netflix, Hulu Plus Live TV, Disney+ and others, according to Horowitz.

With costs on the rise, perceptions of streaming as a better value than cable/satellite are beginning to erode, the researcher reports.

Despite the proliferation of streaming services, 40%

of viewers now agree that they “have a hard time finding something to watch.”

In 2021, 49% without cable/satellite services felt that they were “saving a really good amount

of money” by relying solely on streaming; this year, that number has dropped to 39%.

The study also suggests that churn will become an even bigger challenge for streaming services moving

forward, as consumers become even more cost-conscious.

Nearly one in five (18%) of SVOD subscribers and nearly four in 10 (42%) of those subscribing to a vMVPD now say they’re planning

to cancel at least one of their services.

So what’s next? A reset, according to Horowitz.

“We expect to see more advertising in free or low-cost, ad-supported tiers, such

as the one Netflix is planning to offer, and more consolidation of services and subscriptions, like what just happened with Discovery and WarnerMedia,” says Waterston.

“Hopefully,

for the consumer, this will translate to some cost savings, more predictable spending, and an even better user experience across the board. It will also translate to new opportunities for brands and

advertisers to connect with audiences in new and innovative, interactive ways.”

The State of Pay TV, OTT & SVOD 2022 report is based on a survey of 2,200 heads of households 18 and

older who watch one-plus hours of TV per day.