Netflix still reigns in the U.S. streaming sector,

but it will continue to see some erosion of its dominance in the years ahead, as the field of competitors grows more challenging, according to the latest OTT forecast from eMarketer.

The

forecast, focusing on the major players in the sector, is based on sources including quantitative and qualitative data from research firms, government agencies, media firms and public companies, plus

interviews with top executives at publishers, ad buyers and agencies.

eMarketer estimates that 182.5 million people (55.3% of the U.S. population) will view content through OTT subscriptions

in 2019.

“The market for streaming video has been driven by an explosion in high-end original content and low subscription costs relative to traditional pay TV,” summed up

eMarketer forecasting analyst Eric Haggstrom. “A strong consumer appetite for new shows and movies has driven viewer growth for services like Netflix, Hulu and Amazon Prime Video, as well as the

broader market.”

advertisement

advertisement

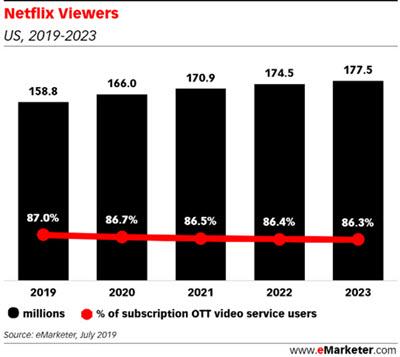

Netflix will draw 158.8 million viewers (over 60.1 million subscribers), for an 87% share, followed by Amazon Prime Video with 96.5 million viewers (53%), Hulu with 75.8

million (41.5%), HBO Now at 23.1 million (13%), and Sling TV at 7 million (4%).

Netflix is projected to see 7.6% viewership growth this year, despite having experienced its first decline in

U.S. subscribers in eight years during this year’s second quarter.

However, its 87% share is down from 90% in 2014, and eMarketer projects that it will decline to 86.3% by 2023.

Meanwhile,

Amazon Prime Video’s 2019 viewership is up 8.8% versus 2018, and is projected to reach one-third of the U.S. population by 2021.

Hulu’s 2019 viewership represents a 17.5% increase

over 2018, although that is down from a nearly 50% growth surge in 2018, largely driven by the success of “The Handmaid’s Tale.”

Although eMarketer doesn’t expect

Netflix to lose subscribers, it does expect the service to find it harder to grow as it increasingly saturates the market and faces new competitors including Disney+, Apple TV+ and HBO Max in the

coming months.

(Netflix CEO Reed Hastings, however, has noted that with an estimated 10% of all U.S TV viewing, the service still has ample room to grow in the domestic market, noted

Deadline.)

“Netflix has faced years of strong competition for viewers, coming from streaming video platforms, pay TV services and even video games,” stated Haggstrom.

“While there is no true ‘Netflix killer’ on the market, Disney’s upcoming bundle with Disney+, Hulu and ESPN+ probably comes closest. Netflix’s answer has been to stick

to what has made it the market leader — out-spending the competition on both licensed and original content, and offering customers a competitive price.”

However, those services

will of course take time to build a subscriber base, and Netflix’s large and expanding library of hit original TV series is a major advantage, he pointed out.

While Disney+ will boast

blockbuster movies, “many of those have already sold to other streamers, and those contracts can last a few years,” so Disney+ won’t have access to its full catalog at launch,

Haggstrom told Forbes.