Now we have not one but two new surveys of advertising

decision-makers that point up the gap between the benefits and promise of connected TV (CTV) and how much is actually being spent on the medium.

A survey of 150 buyers and marketers involved

with digital CTV advertising decision making by Advertiser Perceptions and The Trade Desk (TTD) was highlighted here last week.

This week, the Interactive Advertising Bureau (IAB) released

its 2021 Video Ad Spend and 2022 Outlook study, based on another survey by Advertiser Perceptions (this one with 406 executives who spent at least $1 million on advertising in 2021), plus agency media

spend data from Standard Media Index (SMI).

Both surveys confirm buyers’ growing enthusiasm about CTV.

advertisement

advertisement

As previously noted, among other positive indicators, the TTD-commissioned

survey found 35% of CTV ad buyers saying they plan to increase their CTV allocation during this year’s event compared to last year’s, 61% planning to maintain the same level, and 4%

planning to decrease it.

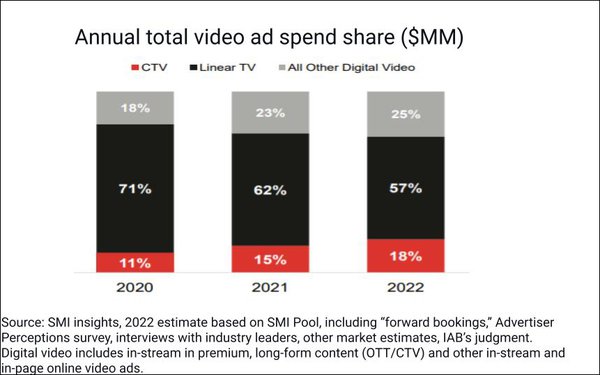

The IAB-commissioned survey provides evidence of several more indicators of CTV’s perceived value.

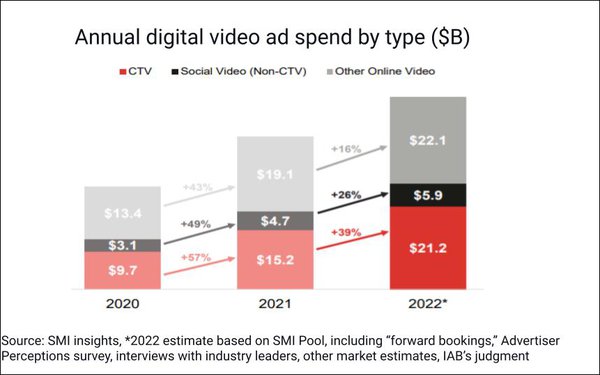

Within digital video, ad investment in CTV is growing

the fastest. CTV spend increased 57% in 2021 to $15.2 billion and is expected to grow an additional 39% in 2022, to $21.2 billion. Between 2020 and 2022, CTV ad spend is projected to more than double

(+118%).

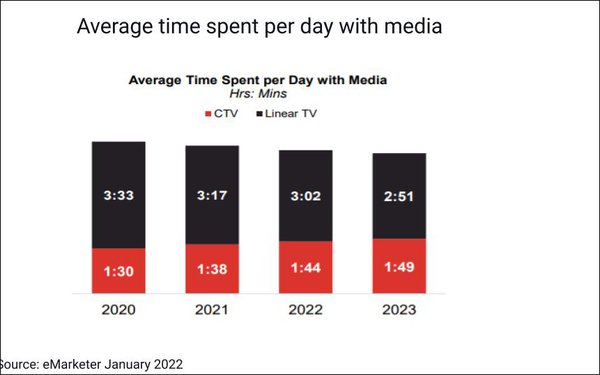

Further, this

year, CTV will account for 36% of total time spent with linear TV and CTV combined.

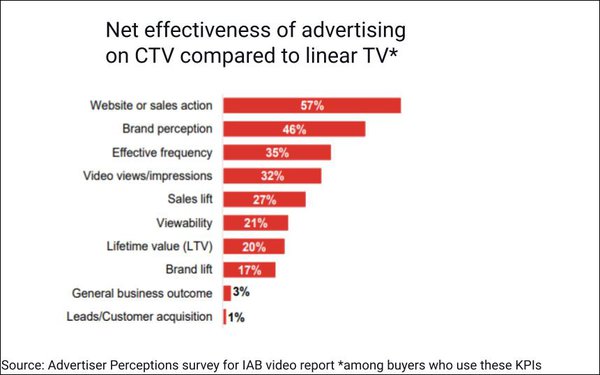

CTV ad spend growth is being driven by multiple factors.

Buyers who use

the common KPIs shown below score CTV as 57% more effective than linear TV at delivering website/sales actions and 46% more effective at delivering brand perception:

CTV enables buyers to leverage many types of data

not available within linear TV buys, including first-party brand data (65% say they use it for CTV), location data (61%), first-party publisher data (60%), video context data (53%), shopping data

(50%), ACR data (35%), weather data (21%), other third-party data (21%) and other second-party data (14%).

Compared to other digital video types, CTV provides more transparency into where ads

run: 59% of buyers said they're “very clear” about where their CTV ads ran, versus only 50% and 43% for social video and other digital video, respectively.

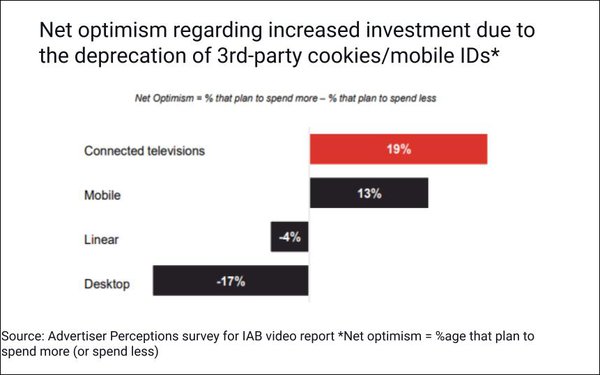

Buyers are turning to

CTV -- which does not rely on third-party cookies -- as a privacy-safe way to spend ad dollars efficiently and effectively. Nearly three quarters (73%) expect to fund their third-party cookie/mobile

ID deprecation CTV spending increases by reallocating dollars from linear TV. (In addition, 46% will fund CTV via overall expansion of ad budgets, 32% by shifting funds from non-video digital ads, 25%

by shifting funds away from social video/digital video ads, and 23% by shifting funds away from other ads.)

This study finds 19% of buyers planning to spend more on CTV specifically because

it's a cookie-free alternative -- and 4% planning to spend less on linear TV in this context.

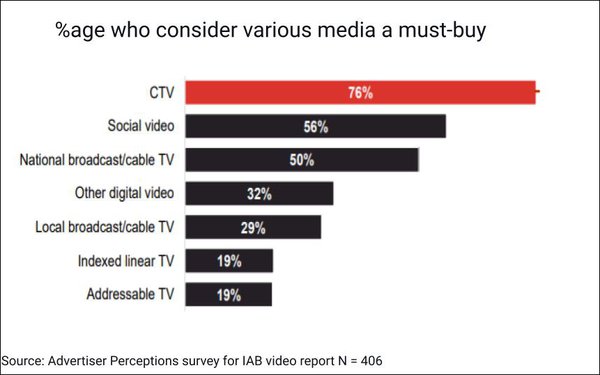

As a result of these benefits, 76% buyers say they consider CTV a "must buy,"

versus just 50% saying the same about national broadcast/cable TV (chart at top of page). And among the largest media spenders, fully 87% say CTV is a must buy.

But here's the

kicker: The estimated CTV spend for this year amounts to just an 18% share of estimated total video ad spend -- far below CTV's 36% share of total consumer TV viewing time.

Why the gap between perception and

behavior?

None of the reasons are new, but it's still useful to take a pulse on them at this stage.

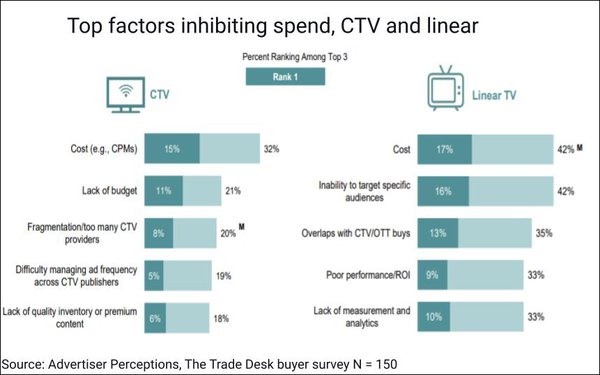

As we'd expect, buyers' expressed reservations or concerns about CTV were similar in

both recent surveys, although the options presented differed somewhat.

Here's a summary of their assessments of CTV's challenges versus linear TV's, from the TTD-commissioned survey:

Respondents to the

IAB-commissioned survey appear to give somewhat less emphasis to CTV's cost factor, and even more emphasis to issues relating to cross-platform measurement and transparency.

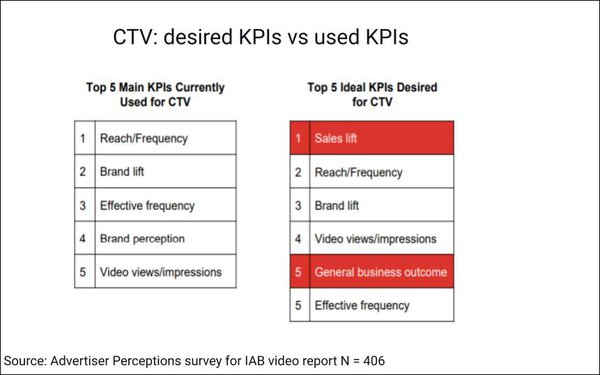

The IAB report

points out that cross-platform challenges including measurement complexity, sub-par tool functionality and data lags inhibit advertisers from using sales lift -- their optimal KPI -- and also general

business outcome, to assess CTV performance.

Buyers say they’re addressing CTV’s challenges in part by preparing for a converged linear TV/CTV marketplace — which 88% believe will happen (42% within the next two

years, 46% longer than two years). Such a marketplace would presumably ease management of cross-platform and cross-channel video buys.

Two thirds (66%) of linear TV/digital video buyers now

have a single planning team for the two channels, and another 25% expect to have one planning team in the future.

Video buyers are also implementing creative and targeting tactics.

Nearly two thirds (64%) report leveraging multivariate creative to help reduce over-frequency and over-exposure to the same ads.

“Continued adoption and fine-tuning of emerging ad

formats will help shift adoption towards CTV,” sums up the report. “Among users of emerging formats, influencer-based and shoppable are performing well across the funnel. These formats are

ripe for CTV, as buyers express that CTV can deliver KPIs more effectively across the funnel than linear TV.”

More than half (52%) are trying to reduce ad fraud by increasing use of

contextual signals to replace open exchange-based audience targeting.

The researchers stress that, for many emerging and established brands, “it’s time to right-size spend”

to reach the growing number of consumers no longer watching traditional television.

They also suggest that more advertisers should use CTV not just for bottom-of-the-funnel performance

campaigns, but for optimizing reach and frequency for branding against light TV viewers, and reaching audiences more precisely on a national or local basis.

To facilitate the strategic shift

to streaming, they recommend reorganizing media agency team structures to bring planning and execution closer together; leveraging innovative smart-TV creative formats; closer collaboration among all

supply-chain parties to prevent poor ad placement; using identity and addressability tech partners to overcome streaming channel fragmentation; and ensuring that their measurement partners are

verified by an independent third party (the Media Ratings Council).

They also caution against relying exclusively on legacy pricing models. “While broadcast/cable TV may appear less

expensive in terms of hitting mass impression targets, the waste that comes with serving ads to unwanted audiences has become part of buyers’ standard calculations to move beyond ‘spray

and pray,’” they note.