Netflix’s loss of 200,000

subscribers worldwide in first-quarter 2022 stunned the industry, suddenly flipping the dominant buzz phrase from “streaming wars” to “streaming recession.”

Perhaps

most disturbing, the overall Q1 loss included a drop of 636,000 North American subscribers.

Further, as reported this week, Netflix’s domestic subscriber losses in the second quarter

doubled, to 1.3 million (although Q2’s worldwide loss of 970,000 was better than the 2 million that Netflix had projected).

But the only truly shocking thing about this trend is that

neither Wall Street or Netflix saw it coming, asserts Michael Greeson, founder and principal analyst of Aluma Insights, which advises creators, aggregators, distributors and others about connected

consumers and their evolving video habits.

advertisement

advertisement

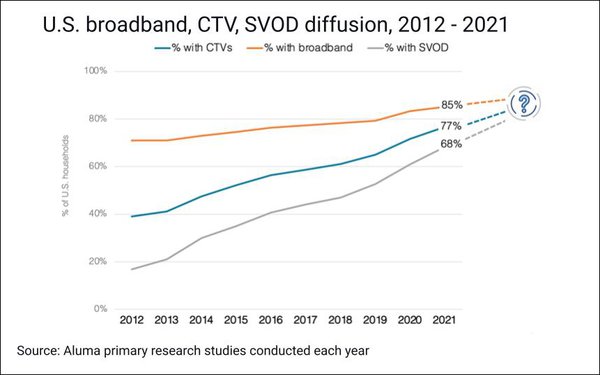

Based on nearly two decades of tracking consumer technology, Aluma started telling clients in 2012 that broadband’s diffusion would set

the upper limit for growth of ancillary industries, so it was important to monitor its ongoing progress.

It was clear that the key structural trends that had long protected consumer

technologies and services from economic downturns would weaken over time — in particular the rapid rates of diffusion, or consumer adoption, for broadband, connected TVs (CTVs) and subscription

video-on-demand (SVOD) streaming services.

Because the expanding base of connected consumers was a boon for those corollary industries, “we argued that where broadband went, so too

would uptake of home networks, wireless connectivity, and broadband-enabled devices and services," Greeson says.

By 2019, the firm was warning that the growth slowdown "was not only

inevitable, but would happen sooner rather than later."

Just 35% of U.S. households had broadband as of 2005. By 2012, that rate had doubled. But in the decade since, growth has been

“painfully incremental,” he points out. “It took COVID 19 to generate a meaningful spike in diffusion.” At year-end 2021, the U.S. household high-speed internet services

penetration level was at 85%.

Mature products and services long dependent on broadband's continuing adoption growth are now bumping up against that saturation (although this isn't, for now, a

strategic issue for newer services like Paramount+ and Apple TV+).

“The vast majority of those wanting broadband and streaming video already have it, and uptake beyond current

levels will be increasingly cumbersome and costly,” sums up Greeson. “The broadband gravy train of the last two decades has mostly run its course.”

Saturation requires a

shift in strategy from growth at all costs to optimizing revenue for the older services, he says.

And that requires changes such as the ones already being implemented by Netflix and others,

including reducing operating costs, converting password borrowers to buyers, adding less expensive ad-free options for consumers, and possibly bundling among disparate networks as well as within a

single network.