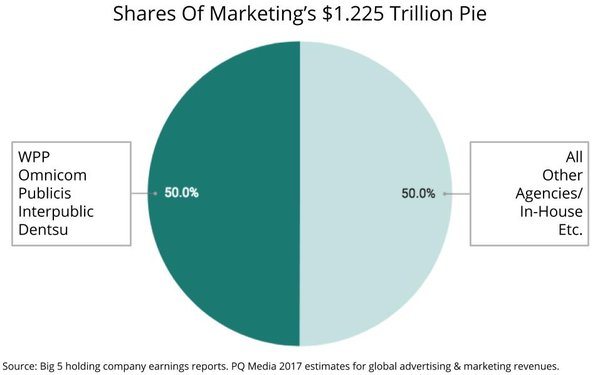

Many in the ad world think of

“Madison Avenue” -- as defined by the big agency holding companies -- as representing a critical mass of the industry, but a back of the envelope analysis by Research Intelligencer

analysis of some current industry estimates shows that the Big 5 (WPP, Omnicom, …

Reminder: You are seeing this premium content because you are a subscriber to MediaPost's Research Intelligencer and/or a member of the Center for Marketing & Media Research. This content cannot be viewed by non-subscribers/non-members.