Weakness in the upfront marketplace appears a foregone conclusion for legacy and digital-first platforms. So what happens after that?

A strong scatter

market? In the old days, that would have been the result. But nowadays? There are a lot more complications in play.

Looking on a granular level, TV ad sellers are attempting

to boost upfront revenue by adding in high-priced sports TV content

-- as well as the usual price additions to one’s traditional cost per thousand viewer (CPMs) prices.

Do you want the ease of programmatic media buying, specific business

outcome results, other first-party data/clean room extras? That will cost you.

Looking more broadly, there is still a major question about the health of the market -- at

least for premium video.

advertisement

advertisement

After experiencing an extended period of steady growth -- with the belief of a recession slowly disappearing in the background -- we still could be facing an

uncertain economy in the near term.

All this comes at a time, legacy TV network-based companies are still struggling to find consistent profitability.

The slow-moving marketplace was expected to some extent. This was accelerated by declines in overall legacy TV gross rating points -- and further complicated by streaming platforms'

CPMs dropping like a stone due to the inclusion of Amazon Prime Video adding an ad-supported option that tossed big ad inventory supplies into the marketplace.

A smaller

contribution of new streaming ad inventory will come from Disney+ and Netflix adding in streaming advertising inventory to the overall marketplace.

Still, some analysts

expect scatter to play a major role in the 2024-25 TV season that traditionally starts in the third week in September.

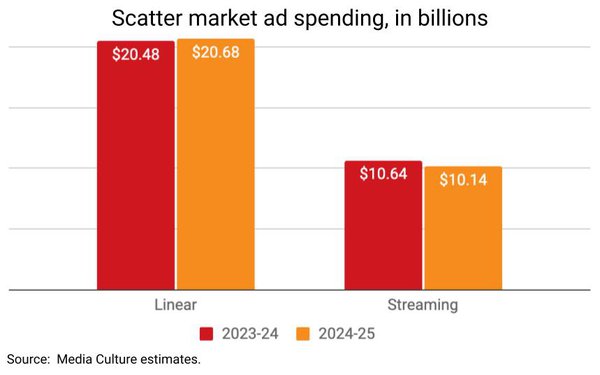

Media Culture, a performance marketing agency,

estimates the linear TV advertising scatter market for next season will barely change -- estimated to be $20.68 million versus $20.48 billion for the 2023-24 TV season.

At the same time, streaming scatter revenue will decline -- to $10.14 billion from $10.64 billion.

The big winner? Streaming inventory sold in the

upfront. It is poised for growth to $18.61 billion, rising dramatically from $13.55 billion.

The bottom line is that a complicated premium TV-video market shows at least

one expected data point that makes sense.

In line with viewing share that continues to rise, brands will boost their upfront streaming advertising coffers right now.