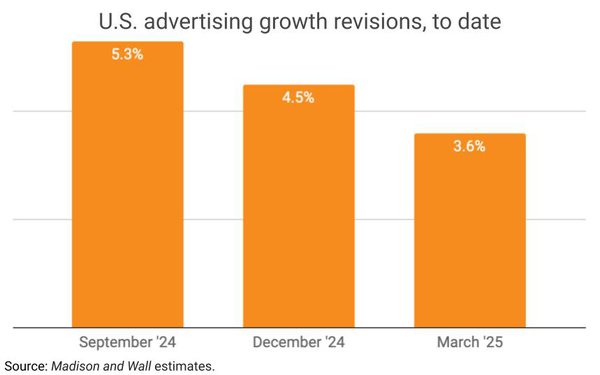

For the second time since benchmarking U.S. ad-growth

projections at +5.3% just six moths ago, ad industry forecaster and publisher Brian Wieser has cut his outlook by nearly a percentage point.

Citing continuing geopolitical turmoil and

uncertainty, Wieser now estimates U.S. ad spending growth will rise 3.6% in 2025, down from his 4.5% forecast in December 2024, and his 5.3% benchmark in September

2024.

Wieser's downward revision comes just ahead of a new quarterly update by IPG Media Lab's Magna forecasting team, expected by the end of this month, and follows allusions of angst and

uncertainty about the geopolitical effects of the new Trump Administration on the overall economy, as well as the advertising marketplace, made by all of the major agency holding company forecasters

-- as well as Wieser's Madison and Wall newsletter -- when they made their year-end predictions in December.

advertisement

advertisement

"By now, nearly three months into the year, what we can see is a

certainty of additional negative factors, including volatility around trade policies and a more extreme threat to supply chains and corporate decision-making than we previously expected," Wieser

writes in this morning's edition, adding: "This has a wide range of consequences for companies, who necessarily become more cautious in their

investment choices, and in for consumers, who shift their resources in order to prepare to negative economic scenarios. If there are any positive considerations for the advertising industry,

it’s that we are not aware of any negative impacts on shipping of goods from China (as Chinese-based cross-border advertisers are a significant source of revenue for Meta and Amazon, at minimum)

and there are not yet any active signs we are aware of indicating that pharmaceutical television ads will be banned."

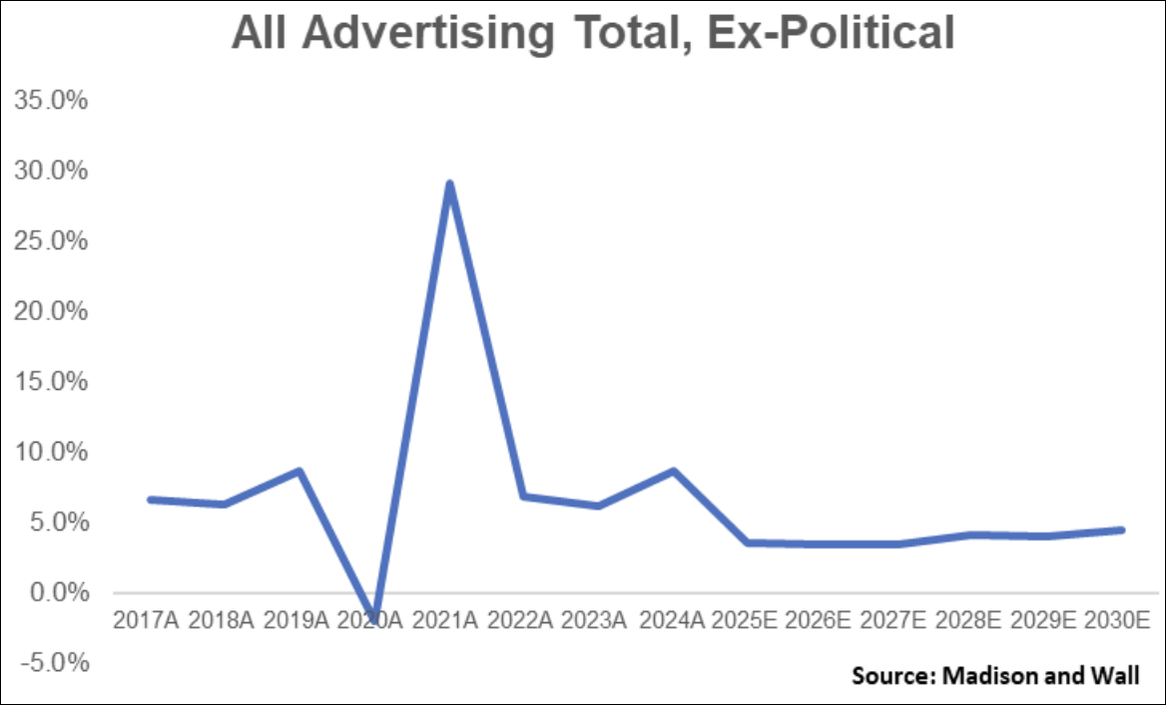

Importantly, Wieser indicates this is not just a short-term correction on

U.S. ad-spending growth for this year, but for some time to come:

"Looking further out, we have generally moderated our growth expectations slightly to better reflect the growth challenges

that are likely to occur if the administration’s policies are pursued as we expect them to be. Overall, our numbers reflect ongoing underlying annual growth of around 3.5% over the next

few years as the economy adjusts to new policies, or slightly softer vs. prior expectations to reflect the generally-more-negative trajectory of the last couple of months. Although this growth

rate isn’t terrible in historical terms, it is below what the industry has become accustomed to, where growth rates were unsustainable. Moreover, if inflation is as elevated as we expect it to

be, it implies limited real growth during this time horizon."