More than ever for this TV upfront

market, brands and media-buying and media-planning executives are focused on one critical factor: real returns on their media spend.

Nearly 50% (45.5%) of respondents to a recent iSpot survey

say it is all about business outcomes.

Farther down on the list is verified ad delivery, with 28.5% pointing to that.

"Outcomes" are listed at the most "significant challenges for

linear and streaming,” at 46.5%, and audience is the next-biggest "challenge" at around 38%.

"Creative" issues registered at 20%, followed by the "efficiency" of a TV/streaming buy at

14.5% and finally, program ratings at 9.0%.

The research goes on to say that 47.5% of marketers expect upfront budgets to remain the same compared to the previous year -- up from 35% heading

into the upfront market a year ago.

advertisement

advertisement

But this "same" budget allocation comes at the expense of linear TV, with a major shift to social video media and CTV/streaming.

Increasingly,

premium TV streaming video content is being combined with social video media, with 24% of respondents saying half of their TV/streaming ads also are placed on social video, while 39% say social video

share will comprise more than half of overall media plans.

More broadly speaking, over 50% of marketers see the rising share of video budgets going to social video and streaming/national CTV

platforms, as national linear and local TV media investments remain the same.

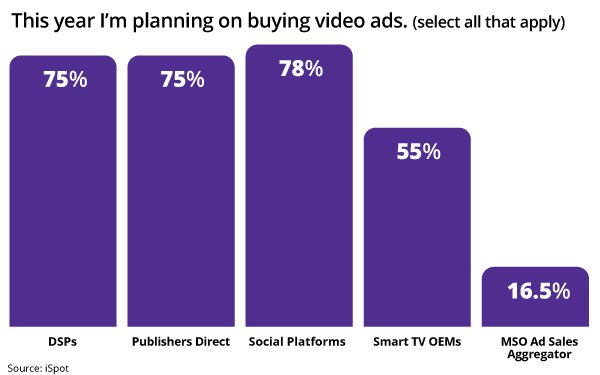

Increasingly, brands are buying video through alternative methods.

Seventy-five percent say they will buy

through publisher-direct platforms, while 78% are planning to buy video ads through social platforms such as YouTube, 75% through DSPs (demand-side platforms); 55% through smart TV operating

system platforms, and 16.5% through multiple system operator (MSO) ad sales aggregators.

The research was conducted with over 200 brand, advertiser, and media agency executives surveyed from

March 25, 2026 to April 27, 2026.