One of the most ironic and surprising developments of

my career covering advertising and media has been the rise of consumers as media -- what we used to call "UGC," or user-generated content, but which nowadays is usually referred to as the "creator

economy."

We can argue about where the line delineating professional from non-professional media content begins and ends, but at least one expert source has put some dimensions around it when

it comes to share of ad spending -- GroupM -- and in its just-released midyear ad forecast update, it provides a fascinating analysis of the share going to user-generated content.

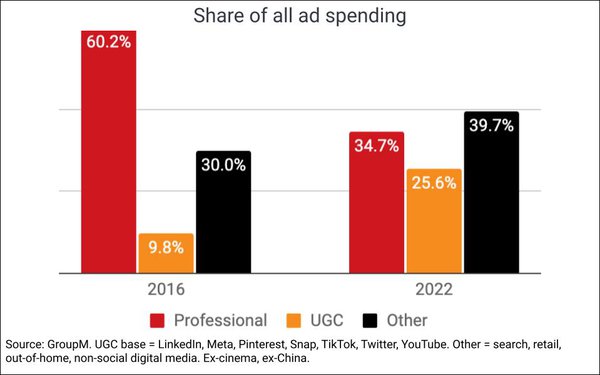

While it's

still a minority, it is approaching the share of ad spending being allocated to all professionally generated media content.

In fact, GroupM found that the share of ad spending going toward UGC

has grown 2.5 times in the past six years, while the share going to professional content has fallen almost in half.

advertisement

advertisement

The only other source to expand and the one that currently dominates the

market is "other," which GroupM Global President of Business Intelligence Kate Scott-Dawkins describes as media platforms not explicitly related to content, such as search, retail, out-of-home and

non-social digital media.

I find the share shift noteworthy, because during much of the early years of UGC there was lots of debate on Madison Avenue -- especially in the trade press -- about

whether UGC would ever be a viable place to advertise.

"Of course, there’s a question as to the amount of content on these platforms that could be considered 'professional',"

Scott-Dawkins writes in the report, noting: "Some content creators have formed sizable media companies with significant revenue streams outside of traditional TV distribution deals. And a recent U.K.

report from Ofcom noted that some teens avoid posting their own content because of the high bar set by influencers. If the content on these platforms is professional in quality and influence (in some

cases), and younger generations are spending more time consuming TikTok than TF1, what’s keeping advertising dollars from shifting more substantially into UGC?"

The biggest potential

game-changer in the category -- as well as many others -- likely will be AI, which already is accelerating the amount of synthetic, non-human-generated content appearing on social media, and elsewhere

(even as "news sites").

"The disruptor in this space is the recent public availability of AI-generated

text and images that enable individuals, media outlets or even bots to quickly and easily produce content that could overwhelm UGC platforms and the open web and make discoverability and verifiability

of content even more challenging," Scott-Dawkins cautions. "Already, any given piece of content may result in claims that it has been written by generative AI, and on the flip side, some posts have

circulated widely before being identified as AI-generated, as in the case of the photo of the pope in a puffer jacket. A new category of advertising services companies to identify AI-generated content

and images will undoubtedly emerge. The added difficulty for advertisers to ensure brand suitability or the potential reputational cost of reacting to issues surrounding deep fakes could delay a

further share shift of advertising revenue away from professional, curated creators and distributors."