Screen and TV media for the first time have tied with billboard

media as the largest asset category with both claiming 29% of spend in the second half of 2024. This reflects the growing weight of video advertising in digital out-of-home (DOOH), according to data

released Monday.

Place Exchange CEO Ari Buchalter shared trends that analysts at the company see for Q1 2025.

Place Exchange, a digital out-of-home (DOOH) and

supply-side platform (SSP), has identified several industry milestones in its H2 2024 Programmatic OOH Trends Report.

"While our next report won't be available until mid-year, we can

share some emerging trends we are already seeing at in Q1 2025," the report says.

-- Traction with omnichannel DSPs - In Q1 2025 witnessed a larger number of omnichannel DSPs spending on

programmatic DOOH than ever before.

advertisement

advertisement

-- In-store retail screens continue to build on the share gained in the most recent report, further driven by spending at and near retail locations.

-- The second-half 2024 report showed that creatives represented half of the spend on video-enabled spend DOOH screens, and early 2025 data suggests that trend will continue, as more brands

leverage the storytelling power of video in the physical world.

The Place Exchange Programmatic OOH Trends report provides a snapshot of select U.S. programmatic OOH spending patterns within

the Place Exchange platform, analyzing delivery across billions of programmatic OOH impressions.

The most recent report compares data from the second half (H2) of 2024 with data from the first

half (H1) of 2024.

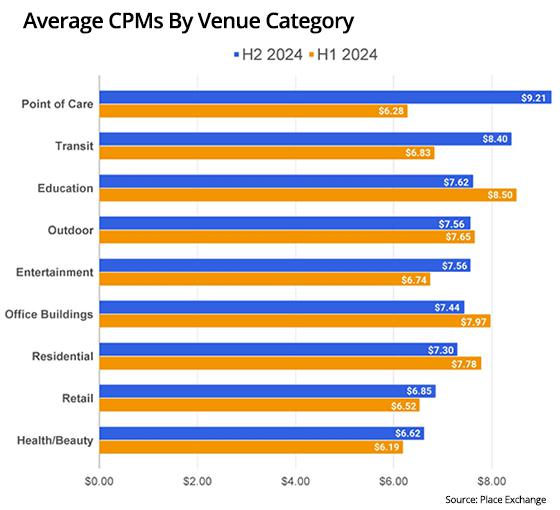

Overall, the average programmatic OOH CPM for H2 2024 was $7.62, nearly 50 cents higher than the $7.16 average in first-half 2024. Point of care, transit, and entertainment

CPMs saw significant increases, while retail and health/beauty venues also saw higher CPMs. The most notable decline in CPM was for the education category.

In second-half 2024, the top three

programmatic OOH advertising categories were food/drink, health/fitness, and personal finance -- collectively growing to 42% of spend.

The fastest-growing categories overall were food/drink,

tech/computing, style/fashion, personal finance, and health/fitness.

The number of unique advertisers on the platform rose 31%, and outdoor -- including billboards and street furniture --

remained the largest venue category, with 52% of spend.

Retail was next at 15%, followed by transit at 11%, and entertainment at 8%.

Overall, the number of programmatic OOH screens

rose 25%, driven mainly by deployments at entertainment, retail, transit, and health locations.

Video ads accounted for half of all programmatic OOH spend on video-enabled screens.

While programmatic OOH supports a wide variety of creative formats, the majority of spending remained concentrated in a few formats.

For example, 15-second video ads remained the most

common duration at 61%, but other common video ad durations gained in share of spend.

Programmatic OOH continued to transact predominantly via private deals, representing 95% of H2 2024 spend,

given the high levels of campaign flexibility, price transparency, and media quality offered to buyers.

Custom private marketplace (PMPs) at 70% represented the majority of spend, while

always-on PMPs made up 23%. Programmatic guaranteed deals, while small, doubled from 1% to 2% of spend.