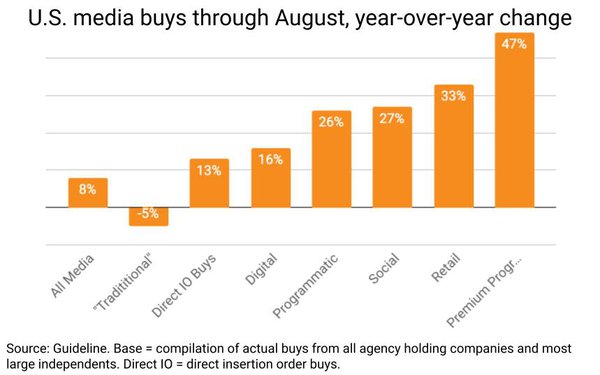

U.S. ad spending

expanded at a healthy 8% rate through the first eight months of 2024, but new

data being released by Guideline (formerly Standard Media Index) this morning shows some sectors -- especially the most "premium" ones -- grew much faster than the rest of the marketplace.

The

data -- which comes from a new "Programmatic Marketplace Insights" report being rolled out by the media-buying intelligence platform -- reveals a markedly stratified U.S. advertising marketplace, with

"traditional" media -- the "linear" kind -- actually declining 5% through August, while the most "premium" kinds are expanding at a much faster rate.

The report does not delineate -- or define

-- what overall "premium" ad inventory actually is, and for my part, I still think that largely is in the eye of the beholders -- on both the buy and the sell sides of the marketplace. But thanks to

Guideline's sophisticated media-buying taxonomy, at least we now know how big holding companies and independent media-buying agencies define premium programmatic media buys.

advertisement

advertisement

And while the new

report doesn't actually delineate the volume or market share of it, it is the fastest-growing segment within Guideline's pool of big agency media-buying data, expanding nearly half as much again (47%)

over the first eight months of the year.

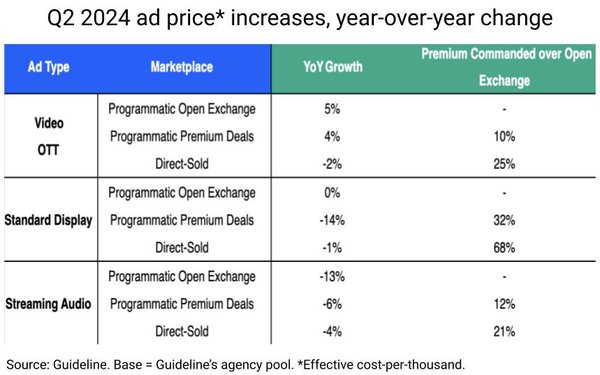

The data reveals that it's not just overall volume growth, but pricing increases as well. (See table below for Guideline data illustrating premium

inventory effective CPM (cost-per-thousand) margin growth for digital video, OTT (over-the-top TV), standard display and streaming audio ad inventory in the open, programmatic direct and direct IO

sold marketplaces during the second quarter of this year.

“When the COVID pandemic hit in March 2020, only a quarter of programmatic investment was bought via premium deals, with open

exchanges dominating the programmatic landscape,” notes Guideline Head of Product Strategy, Direct Solutions Alberto Leyes, adding: “That number has since grown to 48% in the first eight

months of 2024 – posting +47% growth year-over-year – with a projected share of 50% by the end of 2024."

Personally, I've been asking Guideline (previously Standard Media Index)

for this kind of data for nearly a decade, and hope they continue to release some of it publicly so we can continue to provide an objective view of what is driving the advertising marketplace. Because

I agree with Guideline's Leyes when he points out: “Long gone are the days when top content was reserved for direct-sold inventory, and there couldn’t be a better example of this than the

Olympics having been traded programmatically for the first time this year through the agreement between NBCU and The Trade Desk."

In other words, it's not your father's old-school

upfront/scatter media-buying marketplace.