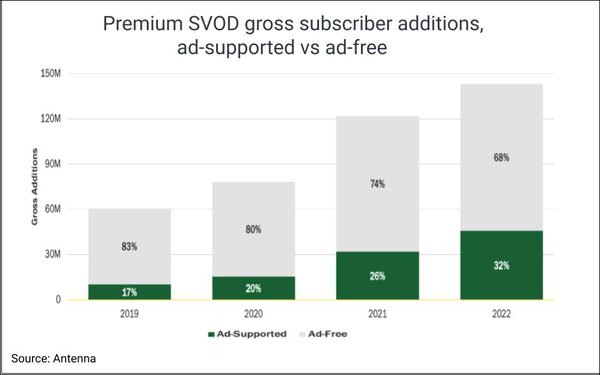

Nearly one in three (32%) of

subscriptions added to premium subscription video-on-demand (SVOD) streaming services last year were to ad-supported plans — up from 20% in 2020 and 17% in 2019, according to the first quarterly

report on subscriptions from Antenna.

At each of the four services that have had ad-supported tiers since their inception — Peacock, Hulu, Paramount+ and Discovery — at least 43%

of total subscriptions are ad-supported. (Ad-supported tiers of paid streamers are often termed AVODs, but Antenna eschews that term.)

Furthermore, the proportion of new subscribers/gross adds

selecting the ad-supported option is higher than the existing subscriber base for six of the seven premium streamers — the exception being Paramount+.

advertisement

advertisement

Another important trend highlighted by the data is the rapidly growing

proportion of subscriptions coming through third parties, or what Antenna calls distribution platforms: Apple, Amazon, Roku and Google. (All of which have their own streaming services or

channels.)

More than half (53%) of new subscriptions came through those platforms last year —up from 44% in 2020.

Apple dominates (27%), in part because a substantial portion of ads through that

platform are for its own Apple TV+.

The nature of distribution deals varies by partner — even ones operated by the same platform, notes Antenna. For instance, the terms for a

distribution platform’s app store could be different than terms in its channels environment.

Direct-to-consumer (D2C) subscriptions allow streamers to keep 100% of subscription revenue

and fully control the customer relationship.

But distribution deals may bring in significant volumes of incremental subscriptions. Also, in environments where services’ programming is

loaded directly into the distributor’s app, like Amazon Prime Video channels, streamers reduce product development and upkeep costs because they don’t have to operate their own proprietary

apps.

Balancing distributor and D2C sourcing is a key factor in determining an SVOD’s model for achieving profitability.

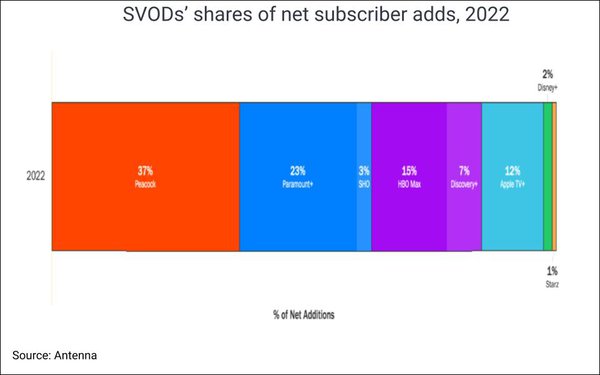

Although newer SVODs are now pursuing profitability and

so stepping back a bit from recent years' overriding focus on achieving subscriber scale, the data show that these Netflix rivals have made substantial progress in attracting new subscribers, with

Peacock and Paramount+ leading the way in 2022.

As a result, entertainment companies’ shares of the streaming

subscription market have shifted considerably.

At year-end 2019, Netflix had a 43% share of subscribers, followed by Disney — including the new Disney+ and Hulu (but apparently not

ESPN+) — at 37%. Warner Bros. (now Warner Bros. Discovery/WBD, with just HBO Max, had the remaining 19%, since NBCUniversal’s Peacock and Apple had yet to launch.

By last year, Netflix and Disney were still the

leaders, but with significantly lower shares. Paramount and WBD now hold 8% to 15% and 6% to 12% shares, respectively, and NBCU and Apple have grabbed 9% and 7% shares.

In addition to advertising streams, the SVODs have

become more aggressive about subscription pricing and bundling in their pursuit of profitability.

Netflix, Apple TV+, Disney+ and Hulu raised sub prices last year. HBO Max did the same in

January, and Paramount+ and Peacock also announced pricing changes in early 2023.

Intra-company bundles are helping to boost average revenue per user (ARPU).

Per Antenna estimates, the

Disney bundle now accounts for 22% of subscriptions for Disney+, 18% for Hulu, and 60% for ESPN+.

The Apple One subscription services program accounts for an estimated 31% of Apple TV+

subscriptions, and subscribers to the Paramount+/Showtime bundle increased by 251% last year, per the report.

Streamers are also being more selective about price promotions and other

revenue-reducing marketing. For instance, free trials’ share of total new sign-ups has dropped from an estimated 46% in 2021 to 38% in 2022, and price promotions declined from 6% of sign-ups on

2021 to 3% last year.