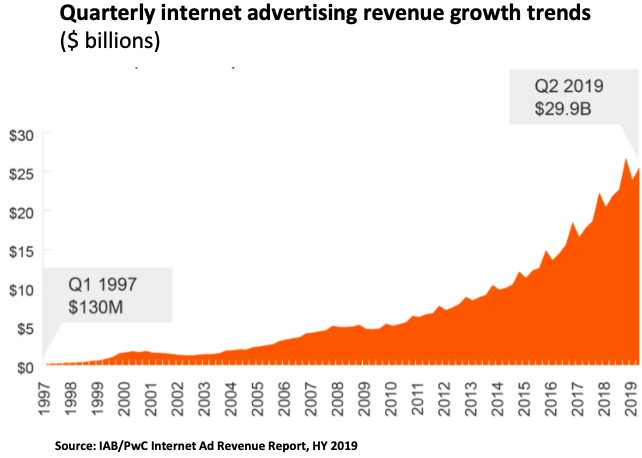

During a briefing on the Interactive Advertising Bureau's and PwC's first half 2019 Internet Ad Revenue Report special guest GroupM President of Business Intelligence

sought to answer questions about why digital's ad growth is beginning to slow down. His answer is it's not yet 100% clear, but it likely is either the maturation of some key drivers -- especially

high-flying growth categories like social and mobile -- or it may just be the economy.

"I do see some macro economic issues being a more practical issue," GroupM President of

Business Intelligence Brian Wieser said during the briefing, noting, "It does feel like we are long in the tooth on economic expansion."

advertisement

advertisement

The big question he said of a macro economic

downturn is explicitly how that might affect digital's ad expansion, given the fact that it was hardly impacted in past economic recessions.

"Does digital media start to behave in

terms of its growth rate more like other media in a downturn, or will it be more resilient?," he asked rhetorically, adding, that he has begun seeing evidence that weakening economies in "other

countries around the world" are showing signs "more meaningful slowdowns in digital," but he said it was too early to see if that might also impact the U.S.

One thing was clear from

Monday's briefing, the rate of digital's growth as begun ebbing in recent quarters, and some of the reasons for that suggested by Wieser, as well as representatives of the IAB and PwC, is that two big

drivers -- social media and mobile -- are beginning to mature and slowdown their rates of expansion.

Eric John, deputy director of the IAB's Video Center of Excellence, noted that

there could be some high growth categories like CTV (connected TV) that currently are not being measured that could actually be propelling digital ad spending growth.

The IAB staff

indicated that they haven't been getting compliance from CTV advertising platforms as part of the IAB's industry self-reported data compiled by PcW.

GroupM's Wieser was more pointed

about the limits of endemic digital advertising growth, noting that two of the biggest recent catalysts -- so-called pure-play digital marketers, and small businesses -- may have maxed out their

incremental impact on the digital ad economy, making the role of traditional big brands a more important driver than ever.

That said, Wieser noted that big traditional advertising

brands already spend about 40% of their media budgets on digital and that it might be difficult to rationalize much more share going that way without some digital "business transformation" case.

He noted that many industries already have done through such transformations.